The biting March wind from the Han River feels even colder today as I stare at the $720 billion black hole appearing on my terminal. I’m leaning back in my Gimpo studio, the smell of dark espresso grounding me as I realize that Big Tech’s AI spending has officially surpassed the annual investment budget of the entire U.S. energy sector. In 2026, we aren’t just building software; we are attempting to build a new planetary nervous system, regardless of the cost.

A cynical deep dive into 2026’s historic $720 billion AI infrastructure spending. Analyze the Capex-to-revenue ratios of Amazon, Microsoft, and Google

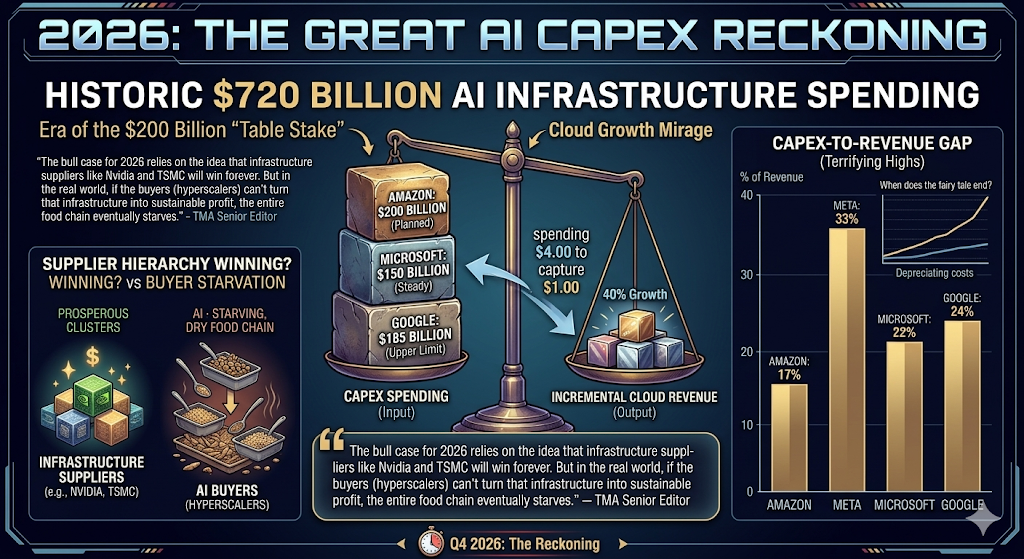

The Era of the $200 Billion “Table Stake”

The numbers for 2026 are no longer just statistics; they are declarations of war. Amazon has dropped a nuclear bomb on the market with a planned $200 billion expenditure—a figure so astronomical the stock fell 9% upon the news. Microsoft is holding a steady $150 billion run rate, and Alphabet is chasing Gemini’s tail with an $185 billion upper-limit guidance.

We have officially exited the “Cost Optimization” era. As I analyzed in The AI Capex Threshold, we are now in an era where Capex as a percentage of revenue is hitting terrifying highs—Amazon is pushing 17% of sales, while Meta is staring down 33%. The question is no longer “Can they afford it?” but “When does the market stop believing in the fairy tale of infinite scaling?”

The Cloud Growth Mirage: 40% Growth at What Price?

Defenders point to the soaring cloud revenues—Google Cloud at 48%, Azure at 39%, and AWS at 24%. It looks impressive on a slide deck. But as a senior editor who has seen three cycles of boom and bust, I see the “Yield War” logic at play. These hyperscalers are spending $4.00 on infrastructure to capture $1.00 of incremental cloud revenue.

Unlike the dot-com era, these companies are generating massive cash flows, which provides a longer runway for their hubris. However, the “Capex-to-Revenue Gap” is widening. We are reaching a point where even a 30% growth in cloud revenue won’t be enough to service the depreciation of the hundreds of billions of dollars in silicon sitting in power-hungry data centers.

“The bull case for 2026 relies on the idea that infrastructure suppliers like Nvidia and TSMC will win forever. But in the real world, if the buyers (hyperscalers) can’t turn that infrastructure into sustainable profit, the entire food chain eventually starves.” — TMA Senior Editor

TMA Fact Check 2026: The Hard Numbers

- The Silicon Concentration: Roughly 75% of the $600B+ combined spend from the Big Five goes directly into AI infrastructure—GPUs, networking, and power management.

- The Apple Exception: Apple remains the outlier, avoiding the “Cloud Arms Race” by focusing on on-device integration. They are absorbing AI costs through high-margin Services revenue rather than building $100B data centers.

- The Energy Sector Parity: The combined AI infrastructure spend of the Top 5 tech giants in 2026 is now 4x larger than what the entire publicly traded U.S. energy sector spends on drilling and refining.

Related Deep Analysis

- The AI Capex Threshold: The Cold Judgment of ROI in 2026

- The Inflection Point: When Will AI Investments Finally Bleed Black?

- The Spoils of Tech Hegemony: Southeast Asia’s Ascent as a Semiconductor Fortress

The Sharp Question

Are you celebrating the “historic growth” of cloud revenues, or are you tracking the Capex-to-Sales ratios that are creeping toward the danger zone? In 2026, the company with the biggest GPU cluster might just be the one with the biggest write-off in 2027.

#Big Tech Capex #AI ROI #Amazon 200B #Microsoft AI #Alphabet Gemini #Infrastructure Bubble #2026 Economy