March 2026 sees a massive reshuffle in the global tech supply chain as the Trump Administration moves to restore tariffs via Section 301 and 232. Discover the macro impact on semiconductors and ASEAN manufacturing.

The “Plan B” Restoration: Section 301 and the Supreme Court Clash

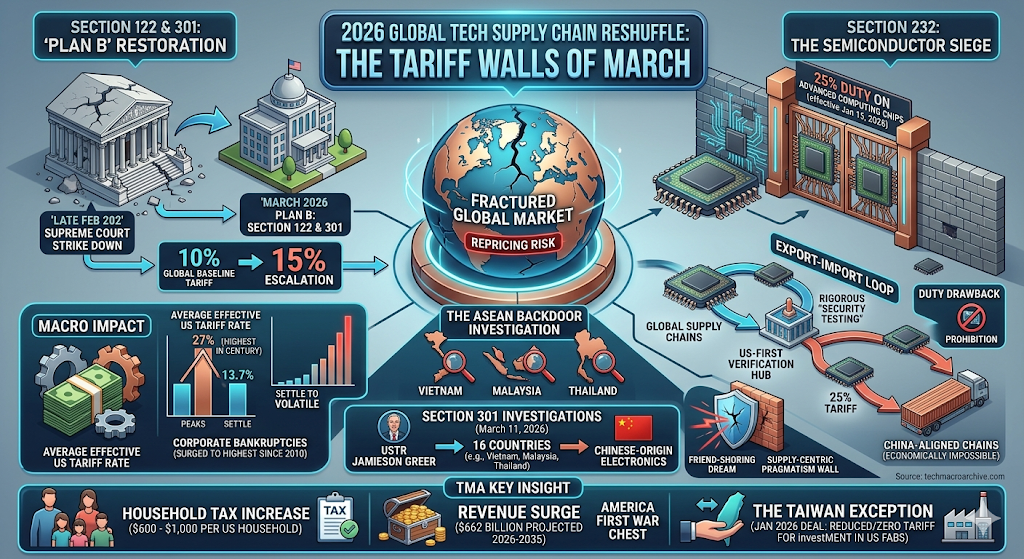

The macro story of March 2026 is one of relentless executive persistence. After the Supreme Court struck down the initial IEEPA-based tariffs in late February, the Trump Administration immediately pivoted to its “Plan B.” By invoking Section 122 (balance-of-payments) and Section 301 of the Trade Act of 1974, Washington has successfully reimposed a 10% global baseline tariff, with plans to escalate this to 15% in the coming months.

For the tech sector, this isn’t just about consumer prices; it’s about Repricing Risk. The 2025 “Tariff Shock” drove the average effective US tariff rate to a staggering 27%—the highest in over a century—before settling into the current volatile 13.7%. The result? Corporate bankruptcies have surged to their highest levels since 2010 as firms struggle to absorb the overhead of a fractured global market.

The Semiconductor Siege: 25% on the “Brain”

The most surgical strike is the Section 232 proclamation on semiconductors. Effective January 15, 2026, an immediate 25% duty was slapped on advanced computing chips and their derivative products. This isn’t just a tax; it’s an Export-Import Loop. Under new BIS rules, chips destined for China must first be imported into the US, undergo rigorous “Security Testing,” and pay the 25% tariff without the right to duty drawbacks. This effectively creates a “US-First” verification hub that makes the cost of routing advanced silicon through China-aligned supply chains economically impossible.

The ASEAN Backdoor Investigation: Closing the Loop

The [Silicon Shield of Southeast Asia] is facing its greatest test. On March 11, 2026, USTR Jamieson Greer initiated Section 301 investigations into 16 countries, including the powerhouses of Vietnam, Malaysia, and Thailand. The target? “Excess industrial capacity” and the use of these nations as “lower-tariff backdoors” for Chinese-origin electronics.

Multinationals that spent 2025 fleeing China for Penang or Haiphong are now finding themselves in the crosshairs once again. The “Friend-shoring” dream is hitting the wall of Supply-Centric Pragmatism. If your factory in Vietnam is using Chinese robotics and Chinese components, the Trump Administration no longer views it as “friendly”—it views it as a target.

“2026 will not repeat the shock of 2025, but it will consolidate it. Companies should assume rising compliance demands and redesign supply chains and pricing accordingly.” — Stafford Powell, Baker McKenzie 2026 Outlook.

TMA Fact Check 2026

- The Household Tax: Current estimates suggest the 2026 tariff regime will increase taxes per US household by $600 to $1,000, creating a persistent inflationary tailwind that is complicating Fed policy.

- The Taiwan Exception: In a strategic play for “Island Sovereignty,” a January 2026 deal offers Taiwanese chipmakers reduced or zero tariffs—contingent on massive, accelerated investment in US-based fabrication.

- The Revenue Surge: Despite legal challenges, Section 232 and Section 122 tariffs are projected to raise $662 billion in revenue over the 2026-2035 period, providing the “America First” agenda with an unprecedented war chest.

Related Deep Analysis

- [The Silicon Shield of Southeast Asia: Vietnam and Malaysia’s 2026 Power Move]

- [The Convergence of Physical AI and Friend-shoring 2.0: Rewiring the Global Factory]

- [The Silicon Iron Curtain: Big Tech’s Brutal Collision with the EU AI Act]

The Sharp Question

As Washington builds a “Tariff Wall” that targets both rivals and allies, are we witnessing the birth of a more resilient domestic industrial base, or are we simply pricing the US out of the global AI race by making the world’s most critical components too expensive to import?

#Trump Tariffs 2026 #Tech Supply Chain #Section 232 #Section 301 #Semiconductor Policy #America First #Tech Macro