The heavy morning mist over the Han River feels as thick as the industrial secrecy surrounding the solid-state breakthroughs of 2026. I’m leaning against the cold window of my Gimpo studio, watching the gray light hit the steel desk. The “Lithium Hegemony” that defined the last decade is about to be rewritten by ceramic electrolytes and lithium-metal anodes. This isn’t just a battery upgrade; it’s a total recalibration of global energy power.

A 2026 deep dive into the geopolitics of solid-state batteries. Analyze how the shift from liquid to ceramic electrolytes is triggering a new global resource wa

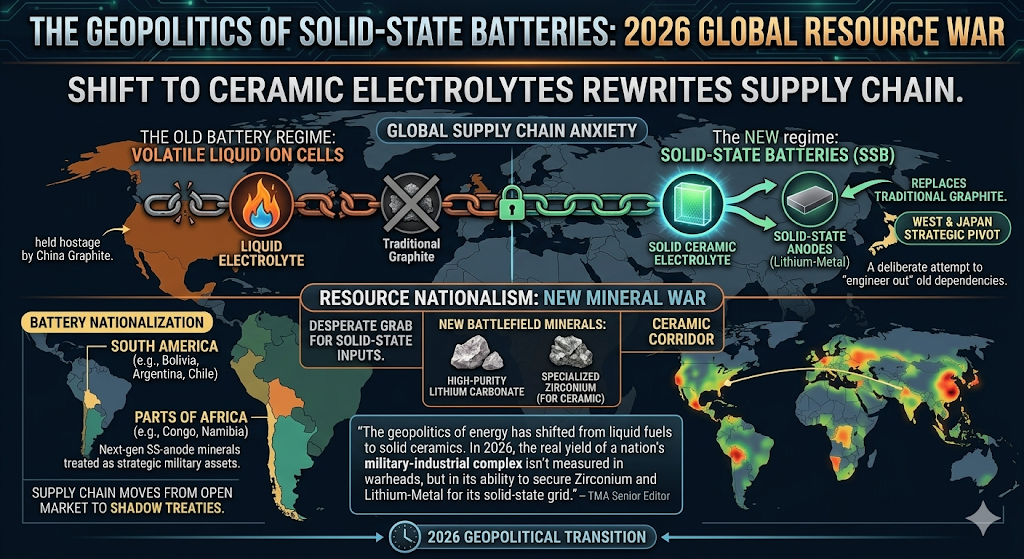

The Death of the Wet Cell: Why Ceramics Change the Map

For years, the EV market was held hostage by the volatile liquid electrolytes of lithium-ion cells. In 2026, the transition to Solid-State Batteries (SSB) has turned the safety and energy density conversation into a geopolitical one. By replacing flammable liquids with solid ceramic or polymer separators, the range anxiety of the early 2020s has been replaced by “Supply Chain Anxiety.”

As I analyzed in Beyond Efficiency, the shift to solid-state allows for lithium-metal anodes, which drastically reduce the need for traditional graphite—a market long dominated by China. This technical pivot is a deliberate attempt by the West and Japan to “engineer out” the dependencies of the old battery regime.

Resource Nationalism: The New War for Solid-State Minerals

The 2026 landscape is defined by a desperate grab for solid-state inputs. We are no longer just fighting over nickel and cobalt. The new battlefield is high-purity Lithium Carbonate and specialized Zirconium for ceramic electrolytes.

Nations are realizing that if they don’t own the “Ceramic Corridor,” they are merely swapping one master for another. We are seeing “Battery Nationalization” in South America and parts of Africa, where the raw minerals required for the next generation of solid-state anodes are being treated as strategic military assets. The supply chain has moved from the open market into the shadows of state-level treaties.

“In 2026, the battery is no longer a component; it is a geopolitical shield. If you control the ceramic electrolyte, you control the mobility of the next decade.” — TMA Senior Editor

TMA Fact Check 2026: The Pilot Plant Reality

- The Mass Production Gap: While “Pilot Lines” are active in Japan and South Korea, true 100GWh-scale mass production is still a 2028-2030 horizon. Anyone claiming total market dominance in 2026 is selling a mirage.

- Yield Rates: The primary bottleneck is “Pressure Management.” Ceramic electrolytes are brittle; maintaining contact with the anode during charge cycles without cracking is the current “Yield War” for battery makers.

- The Cost Premium: In 2026, a solid-state pack costs 4x more than a standard LFP cell. It remains a “Luxury Sovereignty” play for high-end EVs and military hardware.

Related Deep Analysis

- Beyond Efficiency: The Geopolitical Weaponization of the AI Supply Chain

- The Silicon Desert: Mexico’s Ascent as a Strategic Weapon in the AI Yield War

- The AI Capex Threshold: The Cold Judgment of ROI in 2026

The Sharp Question

Are you still betting on the old “Wet Cell” supply chain, or do you see that the 2026 market has already moved to the “Solid State” of sovereignty? If you’re not tracking Zirconium as closely as Lithium, you’re looking at a map of a world that no longer exists.

#Solid-State Battery #EV Supply Chain #Geopolitics 2026 #Lithium-Metal #Ceramic Electrolyte #Tech Macro #Energy Sovereignty