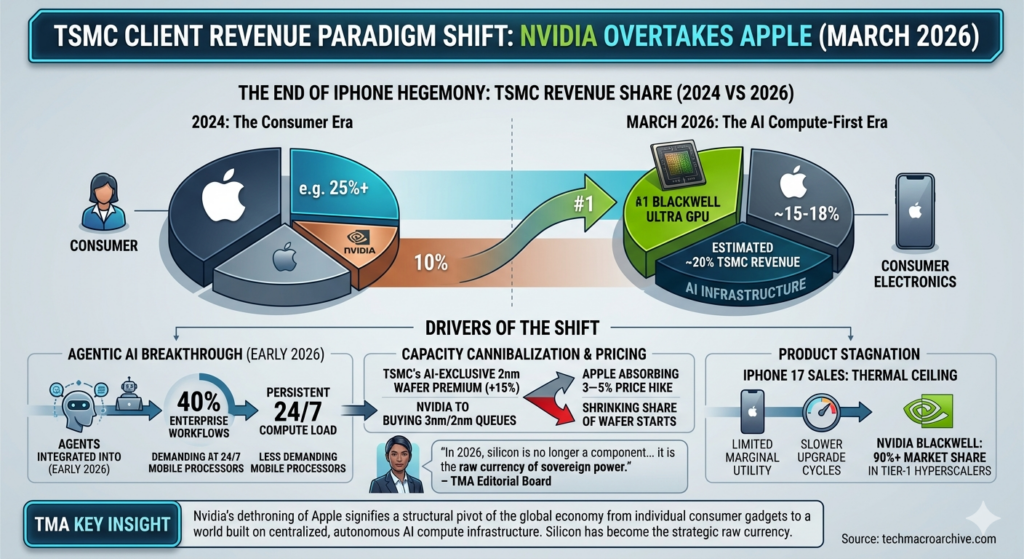

As of March 2026, Nvidia has officially dethroned Apple as TSMC’s largest customer, signaling a definitive shift from consumer electronics to the AI compute-first era.

Data Citation:

According to TSMC’s FY2025 Annual Report and subsequent analysis by Taiwan News, the revenue contribution of Nvidia (Customer A) surged from 12% in 2024 to 19% in 2025, while Apple (Customer B) saw its share contract from 22% to 17%. This marks the first time in over a decade that a high-performance computing (HPC) client has dethroned the iPhone maker.

The End of the iPhone Hegemony

The era of “Apple-first” in the semiconductor supply chain is officially over. As of March 2026, Nvidia has surpassed Apple to become TSMC’s largest revenue contributor, accounting for an estimated 20% of the foundry’s total sales. For over a decade, Apple’s massive iPhone volumes dictated the cadence of Moore’s Law. Today, that privilege has been seized by the insatiable demand for Blackwell Ultra and the upcoming Vera Rubin architectures.

This is more than a vanity metric; it is a structural pivot of the global economy. We are witnessing the final transition from a world centered on individual consumer gadgets to one built on centralized, agentic AI infrastructure.

Analysis: The “Compute-Equity” Trap

Why is this happening now? The answer lies in the Agentic AI breakthrough of early 2026. Unlike the generative AI of 2023, which merely “hallucinated” text, 2026’s AI agents are autonomous workers integrated into 40% of enterprise workflows. These agents don’t just prompt; they execute, requiring a massive, persistent 24/7 compute load that traditional mobile processors simply cannot match.

- Capacity Cannibalization: Nvidia has effectively “bought” the 3nm and 2nm queues, leaving Apple to absorb a 3–5% price hike just to maintain its shrinking share of the cutting-edge wafer starts.

- The Yield Paradox: While Samsung and Intel struggle with High-NA EUV stabilization, TSMC remains the only viable forge. Nvidia’s willingness to pay “compute premiums” has priced out consumer-grade margins.

TMA Fact Check 2026

- Nvidia’s Dominance: Nvidia’s data center revenue continues to dwarf its competitors, with the Blackwell series maintaining a 90%+ market share in Tier-1 hyperscalers.

- TSMC Pricing Power: TSMC has successfully implemented a tiered pricing model where “AI-exclusive” 2nm wafers command a 15% premium over standard logic, a cost Nvidia easily absorbs due to its 70%+ gross margins.

- The Apple Stagnation: iPhone 17 sales have hit a “thermal ceiling,” where the marginal utility of more powerful edge-AI chips is offset by battery and heat constraints, slowing Apple’s upgrade cycles.

Related Deep Analysis

- The Yield War: Samsung’s 2nm Struggle and Micron’s HBM4 Coup

- Algorithmic Sovereignty: Why Nations are Building Sovereign AI Clouds in 2026

- The 300-Watt Phone: The Thermal Ceiling of Edge AI

The Sharp Question

As Nvidia secures the lion’s share of the world’s most advanced transistors to build “Silicon Labor,” will Apple’s pivot to “AI-Native Services” be enough to save its declining hardware relevance, or is the iPhone destined to become the “BlackBerry of the 2020s”?

References: The Historical Shift in TSMC’s Revenue Structure

- [Taiwan News]Nvidia overtakes Apple to become TSMC’s largest client (2026.02.27)

- Key Insight: Analysis of TSMC’s 2025 financial report shows “Customer A” (Nvidia) surging to a 19% revenue share, while “Customer B” (Apple) dipped to 17%.

- [The Chosun Daily]NVIDIA Becomes TSMC’s Largest Customer Amid AI Boom (2026.01.27)

- Key Insight: Reports on the “Golden Cross” where Nvidia’s data center demand officially surpassed Apple’s mobile-driven volume in the foundry’s order books.

- [Bitget Insights]Nvidia Surpasses Apple as TSMC’s Top Client: A New Era of AI Compute (2026.02.27)

- Key Insight: Breakdown of the $23.2 billion revenue contribution from Nvidia, signaling the end of the decade-long “Apple-First” supply chain priority.

- [MEXC Market News]TSMC Stock Analysis: Nvidia Overtakes Apple in Historic Revenue Shift (2026.03.19)

- Key Insight: Discussion on how Nvidia’s willingness to pay premiums for 2nm and 3nm nodes has reshaped TSMC’s pricing strategy and client hierarchy.

#Nvidia #TSMC #Apple #Semiconductors #AI_Infrastructure #AgenticAI #2026TechMacro