Outside my studio in Gimpo, the piercing wind off the Han River estuary remains relentless. I sit staring at the flickering semiconductor market data on my display, nursing the dregs of a now-cold espresso.

While analysts and PR flacks lean on sanitized jargon like “strategic roadmaps” or “technological inflection points,” the reality I’ve witnessed over the years is far cruder. This is a knife fight in a mud pit, where the only metric that carries any weight is yield. That brutal, unforgiving percentage dictates who feasts and who starves.

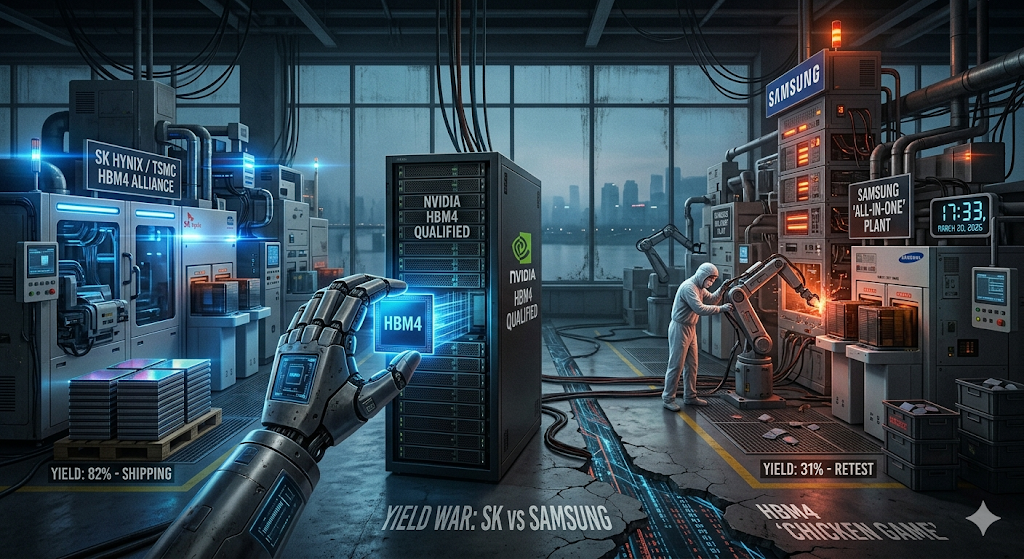

The looming clash over HBM4 (High Bandwidth Memory 4) between SK Hynix and Samsung Electronics is no mere corporate rivalry; it is a desperate, existential chicken game played at the absolute bleeding edge of physics. Forget the glossy brochures. I am here to strip away the marketing spin and dissect the ruthless realities of the 2026 memory wars.

Analysing the brutal HBM4 yield battle between SK Hynix and Samsung. TMA’s Editor-in-Chief breaks down who is winning the 2026 memory war.

HBM4: Stepping into the Technological Quagmire

The HBM market, as we knew it, is over. While HBM3E was an evolution of existing memory processes, HBM4 is a different beast entirely. It’s a Frankenstein monster, fusing memory and logic (system) semiconductors. The crucial shift is the ‘Base Die’ at the bottom of the memory stack, which now must be manufactured using cutting-edge logic processes, typically from a foundry giant like TSMC.

My conversations with industry insiders confirm that this architectural shift has sent production complexity into the stratosphere. This isn’t just about shrinking die size or stacking more layers. It’s about heterogeneous integration—perfectly packaging chips made on radically different processes, managing unprecedented thermal loads, and ensuring signal integrity across tiny connections. The potential failure points are staggering.

The End of Prompting: How Agentic AI and Autonomous Task Execution are Redefining Efficiency in 2026

“The HBM4 production process introduces unprecedented integration complexities, particularly at the advanced packaging stage with the logic base die, making yield ramp the single most critical bottleneck for manufacturers.” — Source: Bloomberg, ‘2026 Global Semiconductor Technology Report’

In this quagmire, the winner isn’t the one with the prettiest lab sample; it’s the one who can drag a sellable product out of the mud. Technical elegance? No one cares. Only ‘volume yield’—the hard, cold percentage of shippable chips—validates a stock price in this market.

SK Hynix: The Sweetness of Dominance, Masked by Dependence

Right now, SK Hynix is the undisputed king of HBM. They are riding high on their exclusive (or near-exclusive) supply deals for HBM3E with Nvidia. Their strategy for HBM4 is simple and seemingly effective: doubling down on the winners. They are deepening their partnership with TSMC, leveraging TSMC’s logic expertise for the crucial HBM4 base die. This is a pragmatic, ego-free play—outsourcing their weakness to the world’s best foundry to focus on their core memory competency.

But I’m not buying the invincible narrative. Hynix’s dominance is brittle. First, they are utterly dependent on TSMC. If TSMC stumbles on the base die yield or faces capacity constraints, Hynix stalls. Second, they have extreme customer concentration. Even if Nvidia loves Hynix today, supply chain diversification is a core tenet of Nvidia’s strategy. They will qualifying a second source.

Third, yield is still the ultimate master. Hynix managed HBM3E yield brilliantly, but HBM4’s process complexity is exponentially higher. Publicly, Hynix may project confidence, but private conversations suggest their internal HBM4 yield targets are causing significant anxiety. The battle for yield is far from won.

Samsung Electronics: A Fallen King’s Flawed ‘Gonjo’

Samsung had a disastrous year in the HBM sector. Failing to qualify HBM3E with Nvidia on schedule was a humiliating blow to the memory giant’s pride. For Samsung, HBM4 is not an opportunity; it’s the final battlefield. Lose here, and their title as the memory hegemon is permanently surrendered. Samsung’s strategy is the polar opposite of Hynix’s: ‘All-in-One.’ They are attempting to do it all—memory, foundry (for the base die), and advanced packaging—entirely in-house.

I see this not as a technological masterstroke, but as a classic example of Samsung’s ‘Gonjo’ (stubborn, grit-driven persistence). It’s a desperate attempt to reclaim past glory by asserting total control and squeezing out yield through sheer corporate will. If it works, it offers superior supply chain agility. But that is a massive ‘if.’ Samsung Foundry’s yield on advanced logic nodes remains a persistent concern. If they struggle with logic yield and memory stacking yield simultaneously, the All-in-One strategy becomes an All-in-One failure.

My sources within Samsung tell me the HBM4 development teams are operating under conditions resembling a constant state of emergency, working brutal hours. This isn’t R&D; it’s manual labor dedicated to yield ramp. Whether this desperation translates into a yield miracle or organizational burnout is a question only time can answer.

Conclusion: Who Walks Away with Nvidia’s Cash?

In the HBM4 yield war, Nvidia is the ultimate arbiter. Their choice between the Hynix-TSMC alliance and Samsung’s All-in-One solution will be based on two unromantic factors: ‘supply stability’ and ‘price.’ And both are functions of yield.

The side with the higher yield can offer stable, high-volume supply and maintain competitive pricing. The side with the low yield faces delivery delays and catastrophic losses. In 2026, the memory market winner will be determined by who has the most ‘shippable HBM4’ sitting in their warehouse.

Outside the studio, the icy wind still howls and hisses, relentless in its bite. As the two semiconductor giants bruise each other in the mud of the yield war, only one thing is certain: the winner’s victory lap won’t be a celebration of technical genius. It will be a gritty sigh of relief for having survived the ugliest yield scramble in memory history.

Fact Check 3

- HBM4 Complexity Explosion: HBM4 introduces unprecedented technological complexity due to the integration of a logic base die and advanced heterogeneous packaging, making initial yield ramp the most significant challenge across the entire semiconductor industry.

- Strategic Divergence: SK Hynix is leveraging an alliance with TSMC for logic die production, focusing on memory excellence, while Samsung Electronics is executing a high-risk ‘All-in-One’ strategy, attempting to control memory, foundry, and packaging in-house for its HBM4 solution.

- Yield-Driven Chicken Game: The 2026 HBM4 market battle is defined not by lab performance, but by ‘volume yield’—the ability to provide stable, cost-effective supply to customers like Nvidia. This has created a desperate yield-squeezing competition where the winner is determined by operational execution rather than pure technical innovation.

The Sharp Question

If you were the CEO of Nvidia, would you bet your AI empire on the perceived stability of a ‘partner-dependent alliance’ (Hynix-TSMC) or the unproven promise of a desperate ‘vertically-integrated monolith’ (Samsung All-in-One)?

#HBM4 #SKHynix #SamsungElectronics #Nvidia #SemiconductorYield #AIChipWar