Hiking up the mountain in the early morning, I stood before a gray sky looming behind the first vibrant sprouts of spring. The green pulse of the earth seemed to hold its breath in the heavy stillness. Now, back at my desk, the fiscal previews for Q1 2026 lie scattered in disarray—the figures are staggering, almost blinding. I sit in my studio, taking a swallow of cold water, and contemplate the widening chasm between the astronomical spending of Big Tech and the actual returns the market is clawing back. It feels as though we are no longer just building data centers; we are erecting massive monuments to a future that has yet to pay its rent.

In March 2026, Big Tech’s AI infrastructure spending is hitting historic levels, led by Amazon’s $200B plan. Dive into the macro analysis of Capex intensity vs. monetization reality.

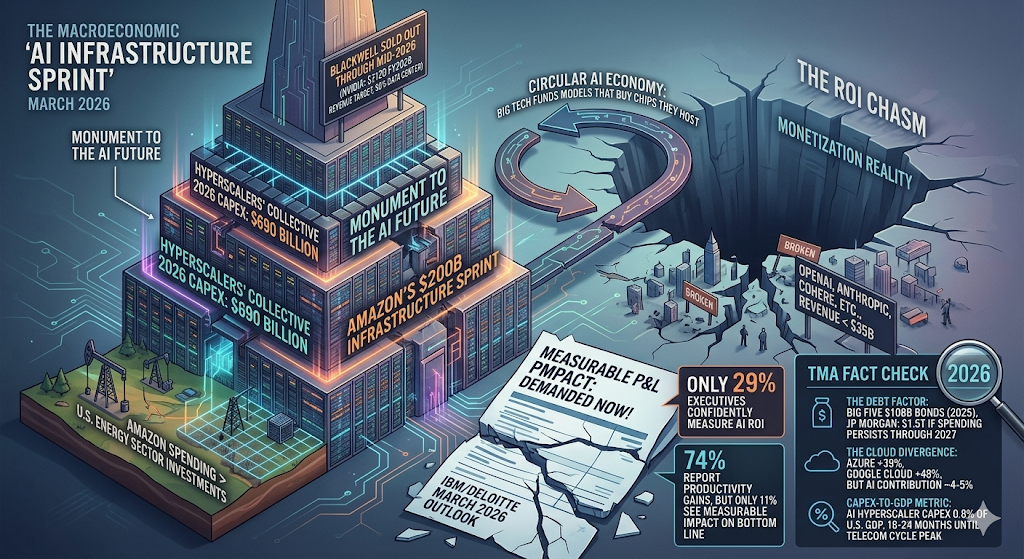

The $690 Billion Infrastructure Sprint

The narrative for H1 2026 is defined by one metric: Capital Intensity. The “Big Five” hyperscalers—Amazon, Alphabet, Meta, Microsoft, and Oracle—have collectively pushed their 2026 CAPEX projections to a staggering $690 billion.

Amazon has shocked even the most bullish analysts with a $200 billion annual spending plan. To put that in perspective, this single company is spending more on infrastructure this year than the entire U.S. energy sector invests in drilling, refining, and grid delivery. This is no longer a growth cycle; it is a full-scale industrial mobilization.

The Blackwell Ramp and the “Demand Gap”

NVIDIA remains the primary beneficiary of this spending spree. In its latest fiscal updates, the company reported that its Blackwell architecture is completely sold out through mid-2026. However, the macro friction is beginning to show. While NVIDIA targets $212 billion in revenue for fiscal 2026—with 90% from the data center—investors are starting to ask the “Sharp Question”: Who is actually paying for the compute at the other end?

The divergence is stark. While hyperscalers are spending hundreds of billions, the combined revenue for pure-play AI vendors (OpenAI, Anthropic, Cohere, etc.) is projected to stay below $35 billion for 2026. We are currently operating in a “Circular AI Economy” where Big Tech funds the models that buy the chips they host.

ROI: From Productivity to P&L

The era of “experimentation first” ended on January 1st. Boards and CFOs are now demanding Measurable P&L Impact. According to IBM and Deloitte’s latest March 2026 outlooks:

- Only 29% of executives feel they can confidently measure AI ROI today.

- 74% report productivity gains, but only 11% have seen a measurable impact on the bottom line.

This has triggered a shift toward Agentic AI as the primary monetization vehicle. As discussed in [The Death of the Assistant], the transition from passive chatbots to autonomous “Digital Workers” is the industry’s last best hope to justify this $700 billion bill.

“A meaningful slowdown in earnings growth could heighten scrutiny and test the market’s tolerance for continued elevated spending… the bar is now higher for qualitative insights on AI inference economics.” — RBC Wealth Management, 2026 Outlook.

- The Debt Factor: To fund this sprint, the Big Five raised $108 billion in bonds in 2025 alone. JP Morgan projects tech debt issuance could hit $1.5 trillion if current spending rates persist through 2027.

- The Cloud Divergence: Azure grew 39% and Google Cloud 48% in recent quarters, but the “Direct AI” contribution to that growth is still estimated at only 4-5%, suggesting that much of the revenue is still coming from traditional cloud migration, not generative inference.

- The Capex-to-GDP Metric: AI hyperscaler capex has hit 0.8% of U.S. GDP. Historically, technology booms peak when this ratio nears 1.5% (as seen in the 1990s telecom cycle), suggesting we may still have 18–24 months of upward runway before a terminal peak.

Related Deep Analysis

- [The Death of the Assistant: Why 2026 is the Year of the Autonomous Digital Worker]

- [The Nuclear AI Renaissance: SMRs as the Ultimate Data Center Hedge]

The Sharp Question

If the “Big Five” are spending $700 billion to build a brain that currently only generates $35 billion in direct revenue, is 2026 the year we realize that AI isn’t just a new tool, but the most expensive speculative bubble in human history—or is the “Agentic Revolution” about to bridge the gap?

#Big Tech Capex #AI ROI #Amazon #Microsoft #NVIDIA Blackwell #AI Monetization 2026 #Tech Macro,