Analysis of the 2026 HBM4 market. How SK Hynix’s dominance in NVIDIA’s Rubin supply chain and South Korea’s 50 trillion KRW “K-NVIDIA” fund are reshaping the global tech-macro hierarchy.

The 2026 Power Shift: SK Hynix vs. Samsung vs. Micron

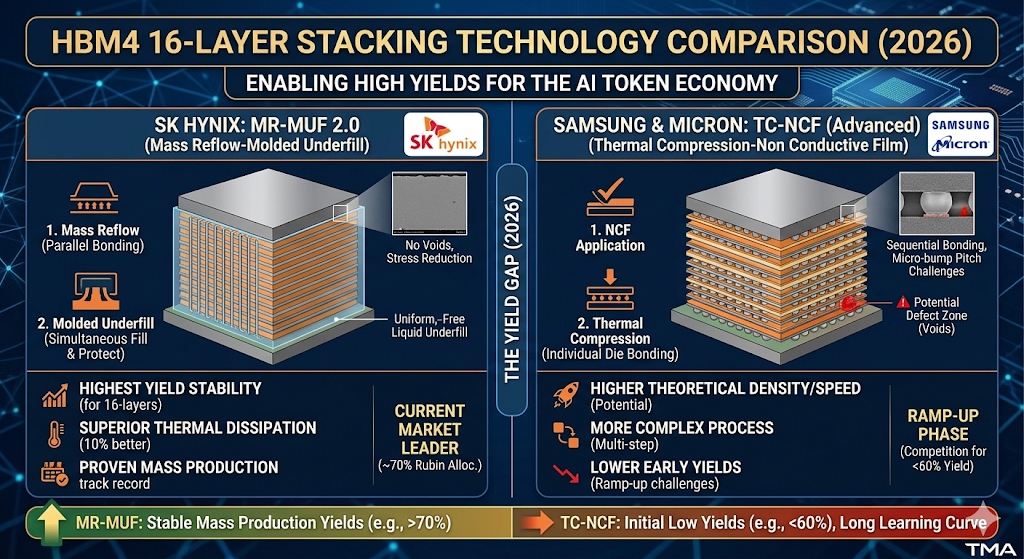

The narrative that dominated 2025—massive CapEx spending—has hit a wall. According to cross-verified reports from Bloomberg and Reuters, the HBM4 market is no longer a monopoly, but a three-way yield war. While Samsung Electronics made headlines by starting mass production in February 2026, SK Hynix has effectively weaponized its technical lead by stabilizing yields for the 16-layer HBM4 faster than its peers.

Table 1: 2026 HBM4 Supply Chain & Performance Benchmark

| Provider | Estimated NVIDIA Rubin Allocation | HBM4 Peak Speed | Current Yield Status (Est.) |

|---|---|---|---|

| SK Hynix | ~70% | 12.5 Gbps | Stable (MR-MUF 2.0) |

| Samsung | ~20% | 13.0 Gbps | Ramp-up (1c DRAM Node) |

| Micron | ~10% | 11.5 Gbps | High-Yield (1-gamma Node) |

Source: TrendForce / BofA Securities 2026 Semiconductor Outlook

The “K-NVIDIA” Subsidy: A 50 Trillion KRW Safety Net

The most critical development for 2026 is the South Korean Government’s “K-NVIDIA Fostering Project.” On March 17, 2026, the Financial Services Commission (FSC) and the Ministry of Science and ICT officially launched a 50 trillion KRW ($37.5B) fund specifically for AI and semiconductors (Chosun Daily Report).

This isn’t just research money. It is “Long-term Patient Capital” designed to:

- Direct Equity Injection: 3 trillion KRW for NPU champions like Rebellions and FuriosaAI.

- Infrastructure Lending: 10 trillion KRW for the Yongin Mega Cluster to ensure power and water stability.

- Risk-Sharing: Acting as a subordinated investor to encourage private equity back into the “Yield-risky” HBM4 segments.

“The 2026 market doesn’t forgive ‘late-movers.’ If you aren’t yielding above the 60% threshold by Q2, you aren’t just losing money; you are losing relevance in the sovereign AI race.”

— TMA Macro Insight, Q1 2026

TMA Fact Check 2026

- NVIDIA’s Rubin Platform: Launching in H2 2026, Rubin will require 8 to 12 HBM4 stacks per GPU, doubling the density from the Blackwell generation (GTC 2026 Highlights).

- Price Surge: Server DRAM prices have surged 60-70% in Q1 2026 alone due to the HBM4 capacity crunch (Korea JoongAng Daily).

- The Yield Gap: Samsung’s 1c DRAM process reportedly offers the highest theoretical speed (13 Gbps), but early yields remain volatile compared to SK Hynix’s mature MR-MUF process.

Related Deep Analysis

- The 2026 Profit Map: Inference TCO and the Copper Bottleneck

- The K-NVIDIA Gambit: Chasing Sovereignty with 50 Trillion KRW

The Sharp Question

As HBM4 becomes a “Strategic National Asset,” will the export controls of 2027 target not just the chips themselves, but the specific Yield-Enhancing Equipment that currently gives Korea its 90% market dominance?

#HBM4 #SKHynix #Samsung Electronics #NVIDIA #VeraRubin #SemiconductorSubsidies #K-NVIDIA #2026TechMacro